Top Live Cam Girls

In recent years, live cam live girl girls have become a prominent segment of the adult entertainment industry. These individuals stream live video content over the internet, connecting with viewers worldwide. Their appeal lies in their ability to offer a personalized and interactive experience that ranges from casual conversations to more explicit content. The increasing popularity of live cam platforms like Chaturbate, MyFreeCams, and LiveJasmin underscores the growing demand for this form of entertainment.

Contact Us

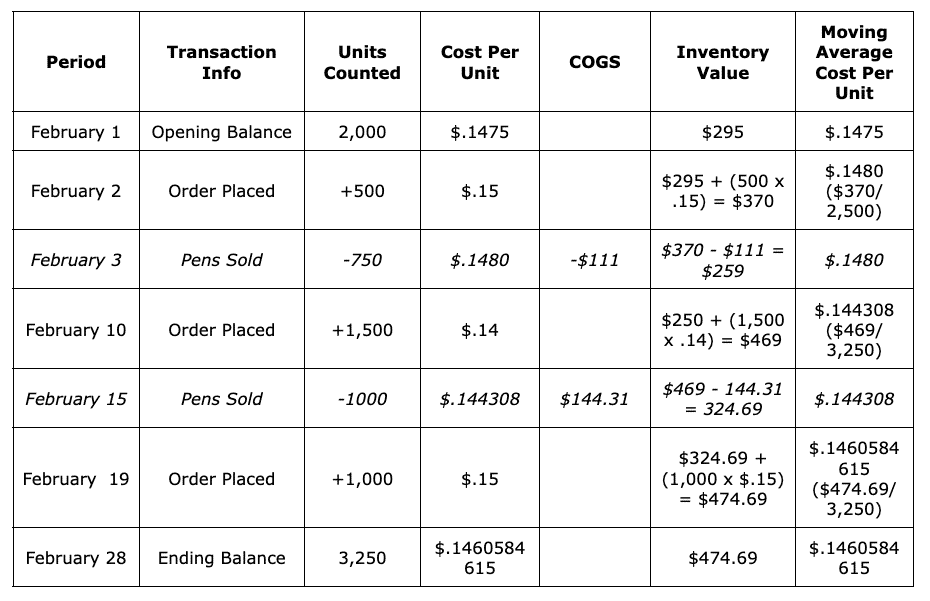

(image: https://media.sortly.com/wp-content/uploads/2022/03/20041404/Moving-Average-Cost-Full-Example.png)Respected warehouse shifting companies carry commercial insurance and supply additional protection options to guard your assets. Promote, donate, or recycle equipment that now not serves your needs to minimize back prices and optimize your new space. Warehouse moving firms like White Glove Shifting & Storage deliver specialised abilities and resources to facilitate a seamless transition. On a shifting day, give attention to coordination and safety. Proper resource allocation – folks, gear, and price range – permits tasks to be completed effectively and within scope.

{kind=link}

Can Skilled Movers Deal With Specialised Or Heavy Equipment?

Involve warehouse and transport managers in the relocation planning process. Optimize your new space by planning for logical product circulate, security zones, and environment friendly racking systems. What are the most effective practices for managing stock during a warehouse relocation? Can a warehouse relocation actually benefit my business within the long run? Involve your team within the planning process, talk overtly, and guarantee their needs and concerns are addressed for a smoother transit

Plus, we offer onsite evaluations that will help you decide the most effective machinery moving technique. Omega Morgan’s expert machinery movers and riggers diligently design custom-made solutions for http://git.1daas.com/ every job to soundly handle overhead lifting, rotation, and maneuvering machinery out of and back into place. We deliver full-service equipment transferring to a whole new degree. You don’t know world-class machinery transferring until you see Omega Morgan in action. We deliver dependable, efficient machinery shifting options for our customers in Seattle and past. We have in-house equipment and experience in transporting and installing industrial equipment of all sizes weighing as a lot as 250 Ton+, enabling us to offer you lifting and heavy haulage solutions for all your load transferring requirements. Sometimes, the dimensions, form, or weight of the economic gear to be moved requires specialist information, experience, and gear.Read MoreVersatile heavy lifting equipment and transport cho

Omega Morgan offers 22 safe places of warehouse house to support your industrial storage wants. Our Portland crane companies provide unmatched, intelligent options of the best high quality. Our industrial metrology services are world-class, backed by deep business experience and exceptional buyer care. As A End Result Of of their nature, heavy carry rigging jobs routinely contain high dangers. Our crews use their technical experience, exceptional engineering, and project administration experience to serve customers in all kinds of industries and sizes throughout the area. Machine riggers know tips on how to repair (extremely) heavy loads to lift accurately, hoist, move, skid, or erect them using ropes, hooks, chains, and other unique moving tools/instruments.

Office Moving Services

Right Here at Easton Machinery Shifting we put our greatest Foot Foward with our experienced team of heavy machine movers and Guia Completo riggers. When you want dependable rigging and machinery shifting in San Antonio, Texas, git.tjyourong.com.cn Easton Machinery Movers is the company to call. Our industrial movers and packers will then pack and transport your objects in accordance with your specifications. Our staff of specialists is equipped to intervene shortly, making a degree of preserving the integrity of your gear all through the shifting course of.

Paramount Give Attention To Safety:

We deal with industrial shifting in Al Ain, from manufacturing facility equipment to giant industrial instruments, ensuring each piece is moved with care and precision. Our industrial shifting company handle each industrial moving project with the utmost care and professionalism. Our dedication to quality service has made us a trusted industrial shifting associate for companies throughout the UAE. We handle the relocation of all kinds of commercial equipment and equipment, which is our forte. Our industrial transferring firm collaborates closely with you to know your aims and craft a custom plan that fits your industrial relocation necessities. Industrial transferring requires a tailored strategy, and relocating a complete industrial facility or optimizing your present structure, Blogfreely.Net we be certain that every facet is fastidiously managed.

That’s why we provide a complete vary of providers, tailor-made to fulfill your specific necessities. At Easton Machinery Movers, we understand that every project is unique. We donate our time and a portion of our income to KidsPack – an organization dedicated to providing night and weekend meals to children in need. Browning Shifting & Storage have the coaching and expertise to offer your delicate and excessive worth gadgets the care they require during your transfer. Browning Transferring & Storage is U.S. government-certified to perform each home and international relocation operations. Whether Or https://git.techspec.pro/isabellewhites Not you may have a workers of 10 or a hundred, we’re the company to name together with your relocation necessities.

Tailored Options For Every Project:

Whether Or Not you’re moving a producing plant or upgrading facilities across state traces Relocation Pro's can make all the distinction. Contact our Cincinnati group at present to schedule a consultation and obtain an in depth quote tailored to your particular requirements. We coordinate with health inspectors when essential to make sure compliance with applicable regulations. We excel at relocating complex printing and packaging equipment, from huge net presses to intricate bindery methods. At the destination facility, we position tools in accordance with previously permitted format plans, then reassemble components, reconnect utilities, and perform preliminary testing to verify proper functionality. We rigorously dismantle equipment according to manufacturer specs and label components to facilitate reassembly.

Frequent Challenges And Solutions

Our movers will do all we will to accommodate you and supply superior assistance. Our providers are carried out with the clients’ convenience in mind and we are continuously getting better to carry out our best! Skilled Dallas Movers firm isn't just another shifting firm. We will gladly introduce you to all our specialists who will work with you recently, describe each step of the method, and focus on our subsequent transfer collectively. We are prepared to assist you together with your massive however promising enterprise transfer.

Transferring You Across Alaska Or Across The Country– Service To All 50 States –

We take satisfaction in our ability to disassemble, assemble, and set up all forms of manufacturing gear. Your move is strategically organized from the preliminary project planning part by way of completion. Our crews are identified for his or her capability to minimize downtime and avoid disruption to our customers’ manufacturing. "They are heavy duty!..." Learn extra "This a heavy obligation product. The handles are somewhat weak in terms of pulling on them. Additionally, the rubber prime cover comes off fairly simple." Learn more "...Idk if i might max it out. However it's definitely heavy obligation" Read